Converting USD to CAD

Converting USD to CAD

Comparison of services and strategies to convert USD to CAD.

Now that your internship in the US is over and you’re back in Canada, how do you convert your hard-earned USD to CAD? There are 2 main things to look out for when converting USD to CAD and vice-versa:

Exchange fee/foreign transaction fee/transfer fee: These refer to the additional fees that the bank/service charges you, typically as a percentage of the total amount.

Exchange rate: This refers to the offered rate that the bank/service is willing to give you, compared to the market exchange rate. The market rate reflects the “true” exchange rate in the public foreign exchange market.

There are many services and strategies you can use, here is a review of the most popular options.

⚖️ Comparison

Cash, directly via bank

This refers to withdrawing USD cash, bringing it across the border, and directly going to a Canadian bank to deposit it. The bank will automatically exchange your USD for CAD.

Please do not do this, this is the worst method for converting your USD to CAD.

On December 1, 2022, the market USD/CAD rate was 1 USD = 1.34 CAD. But looking at various Canadian banks’ currency conversion calculators, they were all giving around 1 USD = 1.30 CAD. Their exchange rates are significantly worse than the market rates.

There’s also usually a foreign exchange fee of around 1-4% added on top of that.

Also note that you’re only allowed to bring at most $10k USD across the border from US to Canada, without needing to report to the US Customs and Border Protection (CBP). This CBP website has more details.

You’re also at risk of misplacing or losing your cash while in transit from the US to Canada.

Credit cards

This refers to essentially not exchanging USD to CAD at all. But rather, if you have a US credit card, once you come back to Canada, to use this credit card to pay for things in CAD. Then you pay your credit card directly using USD. And vice-versa with a Canadian credit card in the US.

Please do not do this if you don’t have a credit card that waives foreign transaction fees.

Since credit cards are usually associated with a bank, you’ll get about the same exchange rate as the bank.

There’s also usually a foreign exchange fee of around 2-4% added on top of that. However, there are some credit cards that waive foreign transaction fees, making this method slightly better than directly converting cash at a bank.

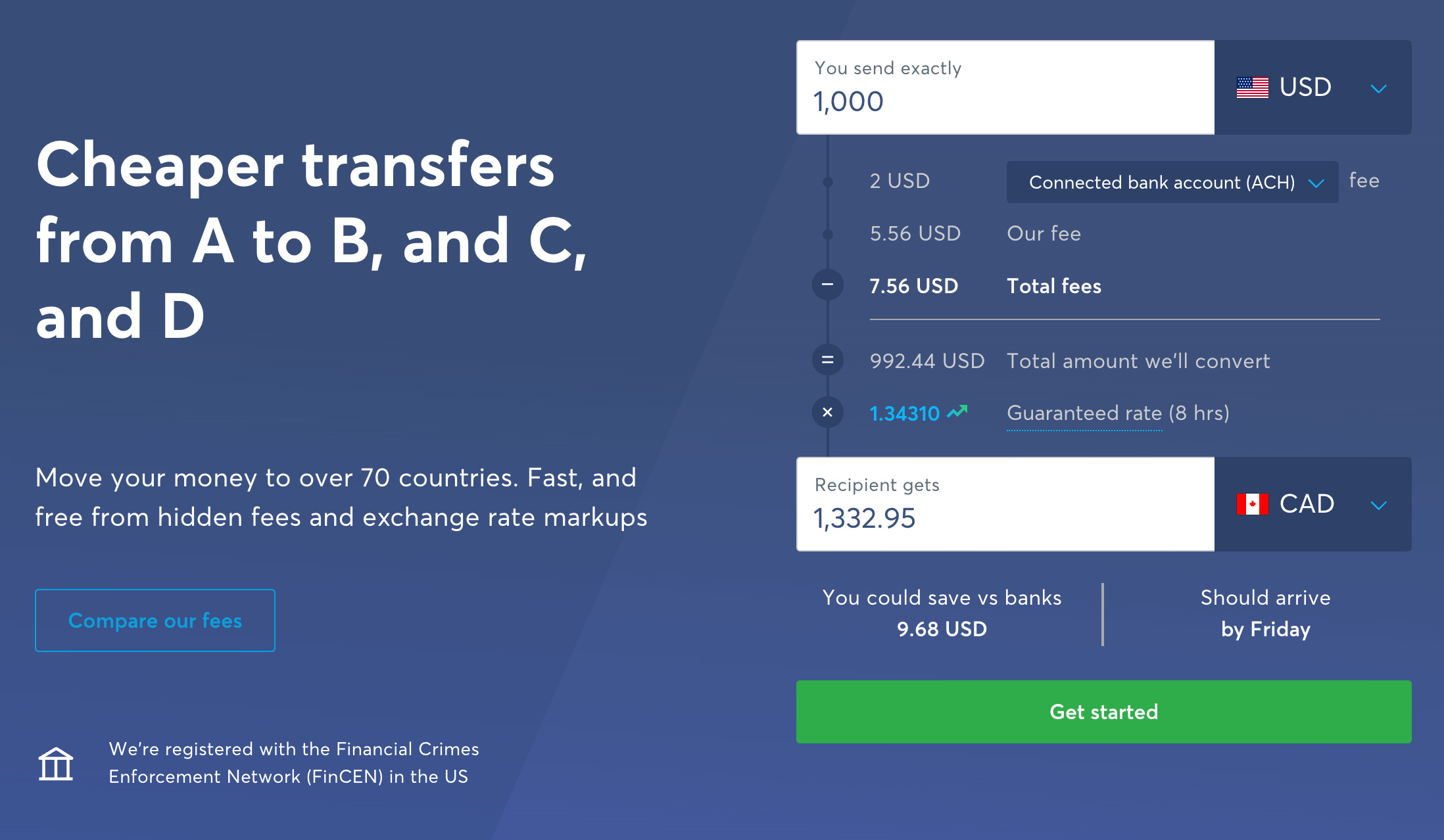

Wise

Wise, formerly known as TransferWise, is a UK-based fintech company used to hold, receive, send, and spend money across 50 currencies and 170 countries. The platform lets you to open an account, link your checking accounts, automatically detect their currency, and enables you to transfer from one account to another while doing a currency exchange.

Wise makes money on their fees, not through exchange rate arbitrage. As a result, the total fees are less than 1% (for transfers of $10k+ USD, total fees are around 0.5%), with about half of that being Wise’s fee, and the other half being the bank transfer fee, which depends on if you’re transferring using ACH, wire transfer, debit card, or credit card. The exchange rate itself is fairly accurate to the market rate.

The exchange rate is guaranteed for 8 hours. This allows you to not worry about fluctuations in the market exchange rate.

They now support 50 currencies, and probably more in the future. This means that you’ll be able to get roughly the same fees and accurate exchange rate for any combination of these currencies. This is very convenient if you’re planning on going outside Canada, for example Europe, after your internship. You can convert your USD directly to EUR, rather than USD → CAD → EUR, in which you’ll pay double the fees traditionally at banks.

The settlement time is about 1-2 days. From our experience, the first couple times you use the service, because you’re a new Wise customer, the transfer time takes around 3-4 days, probably due to security reasons. But after that, you can consistently expect to see the transfer take less than 2 days.

Wise now offers a multi-currency debit card. This allows you to load the account with multiple currencies, and when you use the debit card, it will detect the target currency and automatically deduct from the appropriate currency’s balance. For example, lets say that you load it with USD, CAD, and EUR. When you use the card in Canada, it’ll deduct solely from the CAD balance. When you do the same in France, it’ll deduce solely from the EUR balance.

There’s a referral bonus. As of November 2022, when you invite 3 friends and they transfer more than £200, Wise will you £50 as a referral bonus. More details here, subject to change.

This is our recommended service for doing USD/CAD transfers.

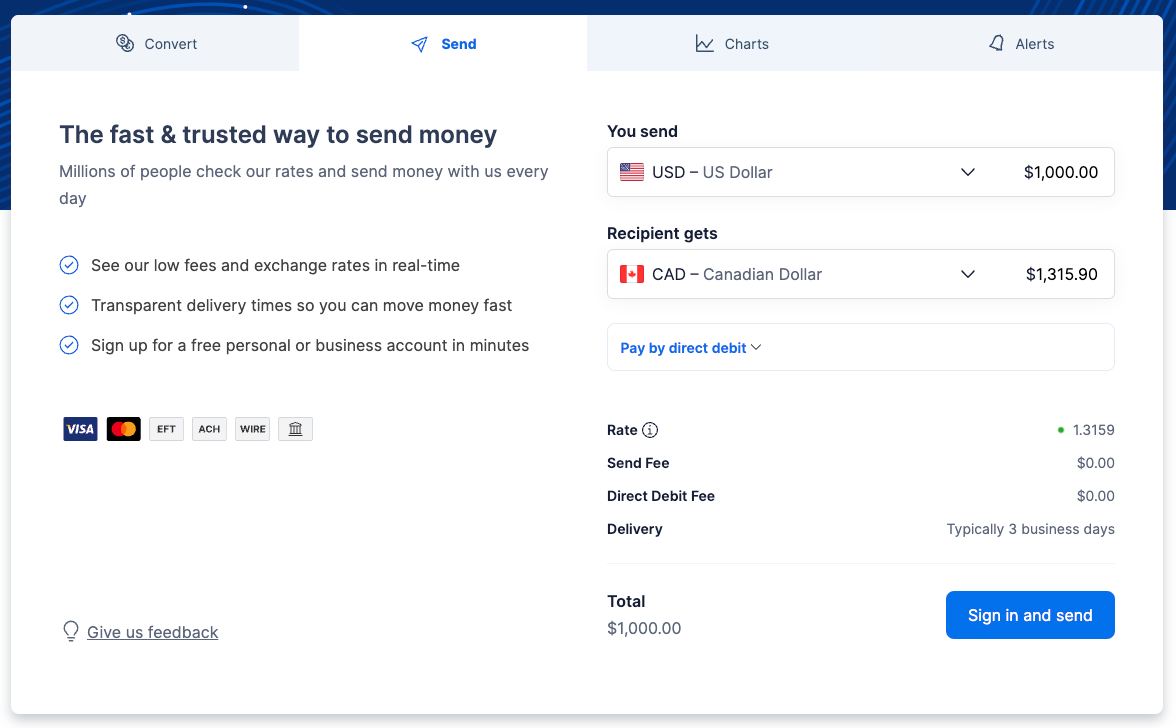

XE.com

XE.com, also known as XE, is a Canada-based fintech company involved in foreign exchange, international money transfers, and currency data/analysis. They support about 100 currencies and 130 countries. The platform lets you to open an account, link your checking accounts, automatically detect their currency, and enables you to transfer from one account to another while doing a currency exchange.

Since XE.com has many commercial customers and is a well-established currency authority (via their real-time Currency API which is used for commercial grade rates), they have much better rates at large commercial volumes for businesses than for personal use.

There are zero fees on transfers by ACH or direct debit, but have 0.5% fees on debit card and 3% fees on credit card. Since XE.com does make money from exchange rate arbitrage, the rate they provide is slightly worse than the market exchange rate.

From our experience, the rates tend to be better for USD/CAD and USD/INR. Overall, they have slightly worse results compared to Wise.

XE.com supports more currencies than Wise.

The settlement time is about 1-2 days. Similar to Wise, the first couple times you use the service, the transfer time takes around 3-4 days, but after it’s consistently less than 2 days.

Cross-border banking

This refers to the fact that Canadian banks like RBC, TD, BMO actually have a US counterpart – a US-based retail banking division targeted towards snowbirds, expatriates, and frequent tourists. They offer cross-border banking solutions such as US checking accounts and credit cards.

For RBC, there’s RBC Bank, based in Georgia.

For TD, there’s TD Bank, based in New Jersey.

For BMO, there’s BMO Harris Bank, based in Illinois.

For CIBC, there’s CIBC Bank USA, based in Illinois.

These subsidiary banks are actual US banks, meaning that if you open a checking account, they can do transfers to and from other US-based banks like Chase or Bank of America, or you can even use them to direct deposit your pay checks.

But since they’re associated with your Canadian account, you can transfer from the USD account directly to the CAD account.

Typically, foreign transaction fees are bypassed, and the transfers instantly settle.

However, the exchange rate itself is just the bank’s rate, which is much worse than the market rate.

Norbert’s Gambit

Norbert’s Gambit, named after Canadian investor Norbert Schlenker, a former retail broker and president of Libra Investment Management, is a method for exchanging USD/CAD sidestepping currency exchange fees at fairly close market rates using stocks that trade in both currencies.

This method has become so popular than an exchange traded fund (ETF) was created specifically for this use.

Open a self-directed account with a Canadian brokerage. Ideally you want to pick a discount brokerage like Questrade or Wealthsimple Trade, which have low to zero commission trading on ETFs, rather than a traditional large bank brokerage like RBC Direct Investing or Scotia iTrade. Trade commissions on Questrade for example are around $4.95 to $9.95.

Buy shares of Horizons US Dollar Currency ETF (DLR.U.TO), which is denoted in USD.

Journal your DLR.U.TO shares to DLR.TO. Both are the same ETF, but while DLR.U.TO is denoted in USD, DLR.TO is denoted in CAD. Journaling refers to the formal method of instead of holding the shares in CAD, to hold them in USD instead. You’ll need to contact your brokerage directly to perform this.

Once your DLR.U.TO shares have been journaled to DLR.TO, sell these shares. This trade will settle in CAD, thereby converting your USD to CAD. You can now withdraw the CAD to a Canadian bank account.

Exchanging CAD to USD is the same process but instead you buy DLR.TO in CAD, journal them to DLR.U.TO, and sell it for USD.

Since traders are able to arbitrage DLR.TO and DLR.U.TO, in theory this method will give you the most accurate market exchange rate for USD/CAD. The fee is fixed (and sometimes free) since you just have to pay the trade commission once on buying and once on selling. However, there are some things to keep in mind:

It takes about 5 days to complete this trade, due to the fact that buying and selling shares take 2 days to settle, and journaling takes 1 day.

This method makes sense if you’re trying to exchange large amounts of currency and are not in urgent need of it.

Within those 5 days, the exchange rate can fluctuate, so you’re not able to get a guaranteed rate like with Wise or XE.com. The rate could move in or against your favor.

✌️ Conclusion

There are many ways to convert USD to CAD and back, here are some key takeaways:

For the most part, Wise is the recommended and usually superior method for exchanging USD/CAD. When accounting for fees and exchange rate, they typically provide you with the best overall rate, inching out over XE.com

Try to minimize the number of exchanges, since there’s a fee in each conversion.

Generally, use a Canadian credit card to pay for things in CAD in Canada, use a US credit card to pay for things in USD in the US, unless you have a credit card that waives the foreign transaction fee.

For the most accurate market exchange rate, try Norbert’s Gambit if you’re trying to exchange large amounts of currency, typically $10k+.

Don’t directly exchange cash, whether USD to CAD or vice-versa.